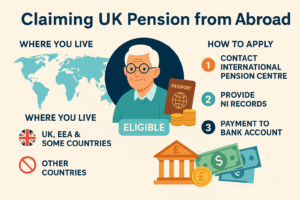

Two Pillars of Retirement in the UK

Retirement planning in the UK is built on two main pension systems: the State Pension and workplace pensions. While both aim to provide income after retirement, they function differently, are funded in different ways, and offer unique benefits.

In this guide, we’ll explore:

- The structure and value of the UK State Pension

- How workplace pensions (including auto-enrolment) work

- The role of employer contributions and tax relief

- How to combine both for a stronger retirement income

1. The UK State Pension at a Glance

The State Pension is a government-guaranteed income that you receive if you have made enough National Insurance (NI) contributions over your working life.

✅ 2025 State Pension Snapshot:

- Weekly amount (full new pension): £221.20

- Annual income: ~£11,502

- Qualifying years required: 35 (minimum 10 for partial pension)

- Eligibility age: 66 (rising to 67 by 2028)

It’s predictable and inflation-protected (triple lock), but on its own, it’s often not enough for a comfortable retirement.

2. What Is a Workplace Pension?

A workplace pension is a scheme set up by your employer. You (the employee) contribute a portion of your salary, your employer matches it, and you receive government tax relief.

🔐 Types of workplace pensions:

- Defined Contribution (DC): Most common; your pension depends on how much is contributed + investment performance.

- Defined Benefit (DB): Less common; based on salary and length of service (e.g., public sector CARE pensions).

3. Auto-Enrolment: What You Must Know

Since the Pensions Act 2008, most employers must automatically enrol eligible employees into a workplace pension.

👥 Auto-Enrolment Criteria (2025):

- Aged 22–66

- Earning £10,000+ per year

- Working in the UK

You can opt out, but staying in means free money from your employer and HMRC.

4. How Much Will I Pay and Receive?

Under auto-enrolment, the minimum total contribution is 8% of your qualifying earnings:

- 5% from employee (including tax relief)

- 3% from employer

| Earnings Band | Contribution (employee + employer) |

|---|---|

| £10,000–£50,270 | Minimum 8% total on income above £6,240 |

| Over £50,270 | Contributions may vary by scheme |

5. Tax Relief: A Hidden Gem

For every £100 you contribute, the government adds £25 as tax relief (if you’re a basic rate taxpayer).

Higher-rate taxpayers can claim even more via self-assessment.

Example:

- You pay in £80 → HMRC adds £20

- Your pension receives £100 instantly

- Employer adds £60 → Total £160 per month

This is a powerful way to grow your fund over time.

6. Combining State and Workplace Pensions

The ideal strategy is to use both pension types to your advantage:

💼 Workplace Pension:

- Flexible, can grow significantly over time

- Investment-based (returns may vary)

- Tax relief and employer contributions add value

🏛️ State Pension:

- Reliable and guaranteed by government

- Indexed to inflation (triple lock)

- Requires long-term NI contributions

📈 Together, they can provide layered security—a base income from the State Pension and a customizable one from your workplace scheme.

7. Pros & Cons: State vs Workplace Pensions

| Feature | State Pension | Workplace Pension |

|---|---|---|

| Source of funds | National Insurance | Salary + employer + tax relief |

| Flexibility | Low (fixed rules) | High (you choose investment, amount) |

| Inheritance benefit | No (unless delayed or married) | Yes (can pass to heirs) |

| Inflation protection | Triple lock (state guaranteed) | Depends on investment choices |

| Maximum income | ~£11,502/year (2025) | No upper limit |

| Access age | 66+ | From 55 (57 from 2028) |

8. What Happens if You’re Self-Employed?

Self-employed workers don’t get auto-enrolment. You must set up a personal pension (like a SIPP – Self-Invested Personal Pension) and manually contribute.

Still eligible for:

- State Pension (if NI is paid)

- Tax relief on pension contributions

9. Should You Contribute More Than the Minimum?

Absolutely—if you can.

Here’s why:

- Employer matches often increase with higher contributions

- Extra tax relief boosts your return

- Compounding over time builds a much larger pension pot

🎯 Target: Aim for 12–15% of your income into pensions for a comfortable retirement.

10. Retirement Strategy Tips (2025 Update)

✅ Start early—even small contributions compound

✅ Maximize employer match

✅ Review annually for fund performance and fees

✅ Consider delaying State Pension for an uplift

✅ Use online calculators (e.g. gov.uk, MoneyHelper)

Frequently Asked Questions (FAQs)

Q1: Can I have both a State and Workplace Pension?

Yes, and it’s highly recommended to do so.

Q2: What happens to my workplace pension if I change jobs?

It remains yours. You can:

- Leave it where it is

- Transfer it to your new employer’s scheme

- Consolidate it into a private pension

Q3: What’s the best pension provider in the UK?

Popular workplace schemes include Nest, The People’s Pension, Aviva, and Legal & General. For personal pensions, look at Vanguard, Hargreaves Lansdown, or AJ Bell.

Conclusion: Secure Your Retirement Through Smart Pension Planning

While the State Pension offers a valuable safety net, it’s not enough to rely on alone. Workplace pensions offer flexibility, tax perks, and significant employer contributions. Combining both systems ensures that you can retire with dignity and freedom.

🔑 Don’t wait—small contributions today = financial freedom tomorrow.

Call to Action

✔️ Use this tool: Check your State Pension forecast

✔️ Log into your employer’s pension portal and check contribution levels

✔️ Subscribe to our blog for weekly tips on pensions, finance, and UK retirement updates